The Roman Extraction

Date: March 2026 Location: Helsinki, Finland — Sam’s Apartment Status: Sam is free. The sauna is 94°C. The Beamer is parked outside. The ultra-silent PC hums at a frequency only dogs can hear. Life is beautiful. Bankroll: Sam: Healthy. Bob: $12,400. Roman: $5,000,000 in the red — and locked in a cell with WiFi.

Roman paid five million dollars to free Sam.

He didn’t mean to. Roman and Sam go way back — they’d swapped pieces, shared Telegram voice notes at 3am, argued about ICM in Discord threads that went on for days. But when Roman walked into The Accountant’s operation trying to settle a debt from a staking deal that went sideways during his downswing, he had no idea that Sam was even in the building. The Accountant — being the kind of man who treats human beings like line items on a balance sheet — simply applied Roman’s $5M payment to the oldest outstanding receivable in the ledger.

That receivable was Sam.

Sam walked out of Cell Block 4 on a Tuesday. Roman walked in on a Wednesday. The Accountant called it “restructuring.” Sam didn’t find out what happened until Bob told him, three weeks later, in a sauna in Helsinki.

Act I: The Sauna Intermezzo

Location: Sam’s building, basement level. Private sauna. Cedar walls. No windows. Perfect.

Sam is on the top bench, pouring water over the kiuas with the focus of a man performing open heart surgery. His skin is the color of a boiled lobster. He has not spoken in four minutes. This is the happiest he has been since 2019.

Bob is on the lower bench, fully clothed, sweating through a hoodie.

Bob: “Sam. SAM. Can you hear me? It’s 94 degrees in here. My phone screen just went black.”

Sam: (eyes closed, voice like a man who has achieved inner peace and a 740 credit score) “This is the optimal temperature for cognitive recalibration. I built an ultra-silent PC, Bob. Custom loop cooling. The fans don’t make a sound. The whole machine runs like a Finnish submarine. I sit in front of it and I can hear myself think for the first time in two years.”

Bob: “Great. Love it. Listen — Roman is in your old cell.”

Sam: (opens one eye) “Our Roman?”

Bob: “Our Roman. The guy who paid five million dollars to The Accountant. The five million that got you out.”

(Sam sits up. The steam swirls around him like a man emerging from a cloud.)

Sam: “Roman freed me? Roman from the Discord? Roman who I swapped 5% with for the WCOOP? That Roman?”

Bob: “His money freed you. And now The Accountant has Roman locked up until he earns it back. All of it. Five million. And The Accountant has rules.”

Sam: “What rules?”

Bob: “Roman has to win the money. Himself. No outside help. No selling action. No staking deals. No swaps. No money from friends. The Accountant says accepting money from other people is ‘cheating.’ Roman has to grind every dollar from the tables.”

Sam: (standing up, towel wrapped, water dripping onto Bob’s shoes) “That is the dumbest rule I have ever heard. And I spent fourteen months in a cell where the guards charged me a 10% ‘technology fee’ on my cashouts.”

Act II: The Accountant’s Dumb Rules

Here is what The Accountant does not understand about poker.

The Accountant is a businessman. In his world, you earn money by doing work. If someone gives you money, that’s charity. If you sell a piece of your action at 1.1 markup, that’s “getting help.” If you swap 10% with another player to reduce variance, that’s “cheating the system.”

The Accountant thinks poker is a salary. You sit down at the table, you grind, you earn. Clean. Simple. Honest.

Uncle Tau has tried to explain.

Uncle Tau: (on speakerphone, sound of 60kg weighted dips in the background) “I told The Accountant: selling action below your EV is not charity. It is smart business. You are converting high-variance future income into low-variance present income. You are paying a premium for survivorship. It is the most rational thing a poker player can do.”

Bob: “What did he say?”

Uncle Tau: “He said, and I quote: ‘If the boy is good enough, he doesn’t need to sell anything. Let him prove it.’”

Bob: “So The Accountant wants Roman to prove he’s good at poker by... making it maximally hard to be good at poker?”

Uncle Tau: “The Accountant does not understand multiplicative processes. He thinks in additive terms. He thinks if Roman is +$50/hour, then in 100,000 hours Roman will have $5,000,000. He does not understand that Roman can be +$50/hour in expectation and still go bankrupt before he ever reaches the mean.”

Sam: “Because tournament poker isn’t a paycheck. It’s a lottery you get to shape.”

Uncle Tau: “Precisely.”

Act III: Shannon’s Demon and the Multiplicative Trap

This is where it gets mathematical. Bob, predictably, did not follow. But this is the part that matters.

Uncle Tau pulled out the whiteboard. (Uncle Tau has a whiteboard in every room of his house, including the bathroom.)

Uncle Tau: “Listen carefully. Both of you. What I am about to explain is why The Accountant’s rules are not just stupid — they are mathematically punitive.“

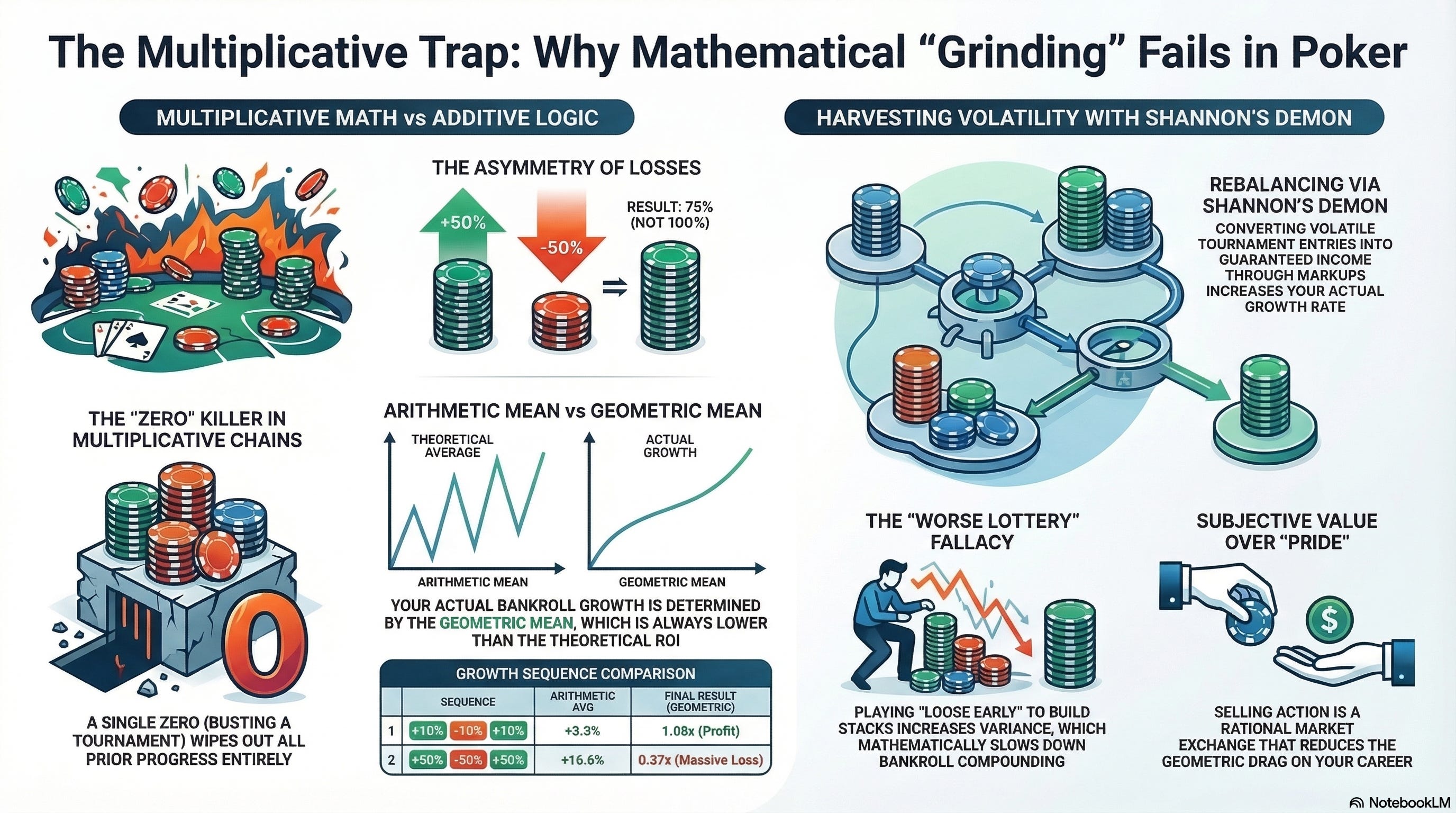

“First: tournament poker is a multiplicative process. Not additive. This single fact explains almost everything.”

Bob: “What’s the difference?”

Uncle Tau: “In an additive process, outcomes stack. You make $100, you lose $100, you’re even. Your results are a sum. In a multiplicative process, outcomes compound. Each result multiplies the previous one. You gain 50%, then lose 50% — you don’t have $100. You have $75. The loss destroys more than the gain created. Every single time.“

“A single tournament is a chain of multiplicative events. Your stack gets multiplied at each stage: ×1.3 when you win a pot, ×0.7 when you lose one, ×2 when you double up, ×0 when you bust. And that ×0 is the killer. In a multiplicative chain, a single zero wipes out everything that came before it. It doesn’t matter if you ran your stack up ×5 in the first three levels. If stage four is ×0, the product is zero.”

Bob: “Okay, but everyone knows you can bust a tournament.”

Uncle Tau: “They know it. They don’t feel it mathematically. Here is what they don’t understand:”

“On any given bullet — any single tournament entry — the process is almost entirely random. You are one player in a field of hundreds or thousands, and the payout structure is shaped like a lottery. Most entries return zero. A few return small cashes. A tiny fraction return life-changing money. The distribution is extremely right-skewed.”

“Now here is the key: when the underlying process is this random — this dominated by variance — a skilled player’s edge shows up as a tiny tilt in a nearly random distribution. You are not flipping a fair coin. You are flipping a coin that lands heads 52% of the time instead of 50%. That is your edge. That is what separates a winning pro from a losing rec.”

Sam: “And in a multiplicative system, a 52/48 edge looks like almost nothing.”

Uncle Tau: “Exactly. In an additive game, a 2% edge compounds linearly. Play enough hands, the edge adds up. Grind, collect, repeat. But in a multiplicative game, the geometric mean is what matters — and the geometric mean is always lower than the arithmetic mean. The more volatile the process, the bigger the gap between what your edge theoretically earns and what your bankroll actually experiences.”

“This is the gap that kills people. And this is what Claude Shannon figured out how to exploit.”

“Shannon — the father of information theory — described a thought experiment that people now call Shannon’s Demon. The idea is beautiful: if you have a volatile asset that goes up and down randomly, you can extract positive growth from the volatility itself — not by predicting the direction, but by rebalancing.“

“You split your capital 50/50 between cash and the volatile asset. When the asset goes up, you sell some to rebalance back to 50/50. When it goes down, you buy. The rebalancing harvests the volatility. In a raw multiplicative process, volatility destroys growth. Shannon’s Demon turns that volatility into a source of growth.”

Sam: “And in poker terms, selling action is rebalancing.”

Uncle Tau: “Precisely. When you sell 40% of yourself at a 1.1 markup, you are doing what Shannon described. You are taking a wildly volatile multiplicative bet — a single tournament entry — and converting part of it into guaranteed income. The markup is your harvested volatility premium. The reduced variance means your geometric mean goes up, even though your arithmetic EV per tournament goes slightly down.“

“This is not weakness. This is not ‘needing help.’ This is the single most mathematically sound thing a tournament player can do. You are running Shannon’s Demon on your own career.”

“But The Accountant has banned it. He has banned selling. He has banned swaps. He has banned every form of rebalancing. He has forced Roman to ride the raw multiplicative process — naked, unhedged, fully exposed to the geometric drag that eats ROIs alive. Roman is Shannon’s Demon in reverse. He is being maximally punished by the very volatility that a smart player would be harvesting.”

Act IV: The Loose Call Problem (Or: Why You Can’t Outrun a Lottery)

Bob: “Okay but Roman is good. He can just play tight and grind, right? Survive early, run deep, cash big?”

Uncle Tau: “And here is the second trap. The Accountant doesn’t just want Roman to win. He wants Roman to win fast. Five million dollars, Bob. At Roman’s current stakes — he’s playing $55 to $530 MTTs off a solar-powered laptop — that is not a grind. That is a sentence.”

“So Roman faces a temptation that every tournament player faces, and that most of them get wrong: play looser early. Take more spots. Get a big stack or die trying. Increase the upside of each bullet by sacrificing survivorship.“

“The logic seems sound: if each bullet is basically a lottery ticket, and you need a massive score to get out of here, why not play for the big stack? Why not take that marginal spot with A9o in the cutoff at 80bb in the first level? If you double up, you have a monster stack and a real shot at a deep run. If you bust, you fire another bullet. What’s the difference?”

Sam: “The difference is multiplicative math.”

Uncle Tau: “Correct. And before we go further, I need to kill a confusion that poisons this entire discussion. There are two things people call ‘ROI’ and they are not the same thing. Mixing them up is how players destroy themselves while feeling great about their results.”

“The first thing: there is the ROI as a belief about your edge. This is the ensemble average — if you could run infinite parallel universes of yourself playing this tournament, what would the average return be? This is your true EV. This is the input to the growth formula. This is what we need to know.”

“The second thing: there is the ROI that Sharkscope shows you. This is the arithmetic mean of your actual outcomes. It adds up every dollar that showed up in your account, subtracts what you spent on buy-ins, and divides by the number of bullets. Money in, money out. Purely additive.”

“Now here is the strange part — the truly strange part that most people never sit with long enough.”

Bob: “What’s strange about it?”

Uncle Tau: “We play a multiplicative game. Inside each tournament, your stack compounds through a chain of multiplicative events — ×1.3, ×0.7, ×2, ×0. Your survival, your chip growth, your path through the field — all multiplicative. But the feedback we receive is additive. Sharkscope gives us a sum. Our cashier page gives us a balance. Our spreadsheet adds up the numbers. We experience the game as a sequence of additive deposits and withdrawals.”

“This is deeply strange. We are playing a multiplicative process and observing it through an additive lens. And the additive lens lies.“

Sam: “How does it lie?”

Uncle Tau: “It lies because two completely different players — with completely different strategies, completely different distribution shapes, completely different geometric growth rates — can produce the exact same Sharkscope ROI. The additive measurement cannot tell them apart.”

“Player A: cashes frequently, grinds small scores, rarely ships but rarely goes on long droughts. Player B: almost never cashes, but when he does, he ships it for huge. Same money showed up over 5,000 bullets. Same additive sum. Same Sharkscope number. 20% for both.”

“But their distributions are nothing alike. Player A has a distribution that is moderately right-skewed. Player B has a distribution that is extremely right-skewed — almost all zeros, with a few massive spikes that drag the arithmetic average up to the same number.”

“And here is why ‘same ROI’ is not just incomplete — it is dangerous. Because you look at your Sharkscope graph and you think: ‘I’m a 20% ROI player. I know my edge.’ But you don’t know your edge. You know your additive outcome history. You don’t know the shape. And the shape is what determines your geometric growth rate — the rate at which your bankroll actually compounds.”

“Player A and Player B both have 20% ROI. But Player A’s bankroll might be compounding at 0.18% per bullet. Player B’s bankroll might be compounding at 0.05% per bullet — or barely growing at all. Same ROI. Three to four times difference in actual wealth accumulation. The additive number is identical. The multiplicative reality is completely different.”

Bob: “So you can’t trust your own Sharkscope?”

Uncle Tau: “You can trust it as a description of what happened. As an additive record of the past. But you cannot trust it as a prediction of bankroll growth. It is not your growth rate. It is not your certainty equivalent. It is the arithmetic mean of your outcomes — and the arithmetic mean of a lottery is only loosely connected to the geometric growth rate of a bankroll that is being bet through that lottery.”

“And this is the part that should make your brain itch: long term, you actually maximize your Sharkscope ROI by having the right distribution shape. Not the other way around. People think: ‘I’ll maximize ROI and the shape will take care of itself.’ Wrong. You choose a strategy that forces a good shape — high survival, moderate variance, consistent cashing — and the ROI follows. Because a good shape means more compounding events, fewer zeros, a higher geometric growth rate. And a higher geometric growth rate means you stay at the stakes where you have an edge, for longer, without going broke. Which, over thousands of bullets, produces the highest arithmetic mean of outcomes.”

“The shape produces the ROI. Not the other way around.”

Sam: “So what we’re actually trying to control is not the ROI number. It’s the shape of the distribution.”

Uncle Tau: “Precisely. We are trying to shape our outcome distribution — through game selection, through strategy, through bankroll management, through selling action — in a way that maximizes geometric growth. And the perverse beauty of this is that maximizing geometric growth also tends to maximize long-run Sharkscope ROI — because the player who compounds his bankroll fastest is the player who stays in the game longest at the highest stakes. But the input is the shape. The ROI is the output. Most people have this backwards.”

“And this is exactly why ‘same ROI’ can be so dangerous. A player can change his strategy — play looser, reshape his distribution — and see the same Sharkscope number for months or years. The additive feedback says: ‘Nothing changed. You’re still a 20% player.’ But underneath, the shape got worse. The geometric growth rate dropped. The bankroll is compounding slower. The risk of ruin crept up. And the player has no idea, because the only feedback he gets is additive, and the additive number didn’t move.”

“We play multiplicatively. We get additive feedback. And the additive feedback is blind to the thing that matters most. This is the central tragedy of tournament poker measurement.”

“Now — every single bullet you fire is a lottery-shaped distribution. Most of the time, you get zero. Sometimes you min-cash. Rarely, you go deep. The distribution is massively right-skewed.”

“Now imagine you play looser early. What happens to the distribution?”

Bob: “You bust more, but when you don’t bust you have a bigger stack?”

Uncle Tau: “Right. So you’re reshaping the distribution. You are taking probability mass away from the middle — the min-cashes, the small deep runs — and splitting it between the far left (more zeros, more bustouts) and the far right (fewer but larger deep runs).”

“Now here is where it gets truly ugly. And this is the part that even smart players get wrong, because it’s counterintuitive. Let’s do a thought experiment.”

“Let’s say — and I’m being generous here — that playing loose early doesn’t change your mean at all. Let’s say, hypothetically, the bigger stacks you occasionally build in the early levels perfectly compensate for the extra bustouts. The arithmetic mean per bullet stays the same. Your ROI, measured naively as total winnings divided by total buy-ins, is unchanged.”

“Bob, would you say the two strategies are equivalent?”

Bob: “I mean... yeah? Same ROI, same edge. What’s the difference?”

Uncle Tau: “The difference is everything. Because you’ve changed the shape of the distribution while keeping the mean the same. And in a multiplicative system, the shape of the distribution matters as much as the mean.”

“Here is what you did: You took a distribution that was already lottery-shaped — already right-skewed, already dominated by zeros — and you made it more lottery-shaped. More zeros on the left. Fatter tail on the right. Same mean, but now the outcomes are more spread out. More volatile. More extreme.”

“You turned a bad lottery into a worse lottery that happens to have the same expected payout.”

Bob: “But wait — if the deep run rate goes up by the same amount as the bust rate, doesn’t it balance out? If I bust 10% more often early but I also go deep 10% more often, isn’t that just... even?”

Uncle Tau: “No. And this is the crux of the entire argument. This is where multiplicative math breaks everyone’s intuition.”

“In an additive system, yes — symmetric changes cancel. You lose $100 more often and win $100 more often, it nets to zero. But in a multiplicative system, gains and losses are not symmetric. A ×0 (bust) and a ×10 (deep run) do not cancel each other out the way +$0 and +$10 do.”

“Here is a toy example. You play 10 bullets. Under Strategy A, 7 survive early and go deep, 3 bust. Under Strategy B, 4 survive and go deep, 6 bust. Suppose the deep runners in Strategy B have proportionally bigger stacks — they go deeper, win more. The arithmetic mean per bullet is the same.”

“But look at the growth path of your bankroll across those 10 bullets. Under Strategy A, you have 7 multiplicative growth events and 3 zeros. Under Strategy B, you have 4 growth events and 6 zeros. Each zero is a ×0. It doesn’t subtract from your bankroll. It multiplies it by zero for that bullet’s contribution.”

“In the multiplicative frame, each additional zero is not just a ‘miss.’ It’s a bullet that contributed nothing — not negative, not slightly positive — nothing. It’s dead weight. And the deep runs that are supposed to compensate? They would need to be multiplicatively larger, not additively larger. To compensate for doubling your zeros, your surviving bullets don’t need to return 2× more — they need to return enough to overcome the fact that you have half as many compounding events feeding your bankroll.“

“The problem is fundamental: adding a bust and adding a deep run of equal arithmetic value to a distribution does not preserve the geometric mean. It always reduces it. Always. The zero pulls the geometric mean down more than the corresponding win pulls it up. This is not an edge case. This is a law of multiplicative dynamics.”

Sam: “So the distribution is asymmetric even when the changes look symmetric.”

Uncle Tau: “Exactly. And this is why you must always err on the side of less variance when you’re operating in a multiplicative system. There is no scenario where making the distribution more extreme — even ‘symmetrically’ more extreme — improves your geometric growth. The zeros always win. The deep runs can never compensate in geometric terms for the additional busts, no matter how big they are.”

“This brings us to the formula. Shannon’s Demon runs on it. Kelly sizing runs on it. Everything runs on it.”

“The optimal geometric growth rate of your bankroll is:”

g = μ² / (2σ²)*

“Where μ is your arithmetic mean return per bullet — your Sharkscope ROI — and σ is the standard deviation of your per-bullet results. That’s it. That governs how fast your bankroll actually grows. And it tells you everything.”

“First thing to notice: μ must scale linearly with σ to maintain the same growth rate. If your standard deviation goes up 25%, your ROI must also go up 25% just to break even on bankroll growth. Not by a little. By the exact same proportion.”

“Second thing: the formula also gives you your Kelly bankroll. The number of buy-ins you need is σ²/μ. More variance, bigger bankroll required.”

Sam: “Put real numbers on it.”

Uncle Tau: “Real numbers. A solid MTT player. Tight early strategy: survives the early levels about 70% of the time, cashes at a moderate clip, 20% ROI. Standard deviation of about 3.4 buy-ins per bullet. Plug that into the formula:”

“Growth rate: 0.20² / (2 × 11.3) ≈ 0.0018 per bullet. Kelly bankroll: about 57 buy-ins. Over 1,000 bullets, his bankroll grows roughly 500%. That is a healthy, sustainable grind.”

“Now. Same player switches to loose early. Survives only 50% of the time — but when he survives, he has bigger stacks, goes deeper. And we’re being generous: we assume the ROI stays exactly 20%. Same Sharkscope number.”

“But the standard deviation jumped from 3.4 to about 4.2 buy-ins. A 25% increase in σ. Variance from 11.3 to 17.6.”

“New growth rate: 0.20² / (2 × 17.6) ≈ 0.0011 per bullet. New Kelly bankroll: 89 buy-ins.”

Bob: “Same ROI though. What changed?”

Uncle Tau: “Everything. Same Sharkscope ROI. Same 20%. But his geometric growth rate dropped by 35%. His bankroll compounds a third slower. Over 1,000 bullets: 500% growth became roughly 200% growth. Same additive ROI. Radically different financial outcome.”

“And his required bankroll jumped from 57 buy-ins to 89. A 55% increase. He needs more capital to play the same stakes at the same risk of ruin — capital that The Accountant won’t let Roman access.”

“To get the growth rate back to where it was, he would need to increase his ROI from 20% to 25%. A 25% relative increase — from a bigger stack in the early levels where ICM pressure barely exists and blinds are tiny.”

Bob: “Is that a lot? 5 extra points of ROI?”

Uncle Tau: “Bob, 20% ROI already represents outperforming a nearly random multiplicative process through thousands of tiny edges — preflop ranges, sizing decisions, population reads, ICM awareness — accumulated over every stage of the tournament. Adding 5 points means increasing your total edge by a quarter. From a bigger stack. In levels 1 through 4. Where the ‘big stack advantage’ is real but marginal.“

“The realistic benefit — wider ranges, some fold equity, slightly better survival through the bubble — adds maybe 1 to 2 points of ROI. Maybe 3 if you’re wildly optimistic. You need 5. And that’s in the generous scenario where the arithmetic mean didn’t change.”

Sam: “And in reality the mean drops too.”

Uncle Tau: “In reality the mean drops too. Those extra bustouts aren’t free. Busting 50% instead of 30% means 20% more bullets that return exactly negative one buy-in. To keep the arithmetic mean at 20%, the surviving 50% would need to average 2.4× their buy-in — versus only 1.7× for the tight strategy. That’s a 40% increase in conditional payout. Which requires not just bigger stacks but significantly better play with those stacks. The numbers don’t work.”

“So the honest accounting: playing loose early, dropping survivorship from 70% to 50%, most likely lowers your arithmetic ROI AND increases your variance. Both sides of the formula get hit. The growth rate doesn’t just drop by a third — it might drop by half or more. And to get back to where you started, you’d need an ROI increase that is somewhere between ‘implausible’ and ‘extremely optimistic.’”

Sam: “So the argument reduces to a single question.”

Uncle Tau: “Yes. For any loose early play decision, the burden of proof is on you: ‘Do I believe this increases my ROI by at least X% to retain the same geometric growth rate?’ The formula tells you exactly what X is. It is proportional to the standard deviation increase. Going from 70% to 50% early survival is roughly a 25% jump in σ, which demands a 25% jump in ROI. That is a massive burden. And the realistic edge from a bigger stack in the early levels — 1 to 3 points — cannot carry it.”

“The implication: in a multiplicative system, you must always lean toward less variance. The heavier you go early, the bigger your ROI must be to justify it. And the gap between ‘what loose play gives you’ and ‘what it needs to give you’ is never small. It is always a losing trade.”

Sam: “So Roman can’t play loose to speed things up.”

Uncle Tau: “Roman would need to believe that playing loose early bumps his ROI by 25% relative. That’s 5 points from having a big stack in levels where the blinds are 50/100 and the average pot is two big blinds. He does not believe that. Nobody who has done the math believes that.”

“The Accountant’s rules have trapped Roman in a Kelly-constrained grind with no rebalancing tools, no acceleration path, and a distribution shaped like a lottery that he cannot reshape without making it worse. The only mathematically sound strategy is: play tight. Preserve the shape. Don’t make an already-bad lottery worse. Let the geometric mean do its work over thousands of bullets. And wait.”

Bob: “That sounds like prison.”

Uncle Tau: “It is prison, Bob. That’s the point.”

Act V: The Machine in the Cell

Meanwhile, 4,000 miles south, Roman is grinding.

The solar panel charges the battery between 6am and 2pm. The WiFi signal is strongest between midnight and 5am, when the guards stream less football. This gives Roman roughly a five-hour window to play, on a laptop that overheats every forty minutes and must be cooled with a damp cloth.

He is playing $55-$530 MTTs. Pure Kelly. No selling, no swaps, no backing. Every dollar he wins goes to The Accountant’s ledger. Every dollar he loses comes off his own hide.

At his current earn rate, optimistically, he will be free in approximately... a very long time.

He sends Bob a voice note every morning:

“Day 49. Battery held at 78% today. Got deep in the $530 Bounty Builder but the WiFi dropped during a 3-bet pot on the bubble. I think the guard was streaming the Champions League. I offered him 5% of my next cashout to switch to radio commentary. He countered at 8%. We settled at 6.5%. I told him I was applying ICM to the negotiation and he had no idea what I meant but respected the confidence.”

“I almost took a loose spot with A5s in the hijack in the first level today. Stack was 100bb. The fish in the big blind had been calling everything. I wanted to isolate him, build a big stack early, accelerate the timeline. Then I heard Tau’s voice in my head: ‘A dead player’s growth rate is zero, forever.’ I folded. I folded A5s in the hijack at 100bb. This is what prison does to a man.”

Act VI: The Debate

Back in Helsinki. The sauna is cooling. Sam is at his grind station — three monitors, the silent PC, a cup of something Finnish and black.

Sam: “We have to convince The Accountant to let Roman sell action.”

Uncle Tau: (on speaker) “I have been trying. The man has the financial literacy of a parking meter.”

Bob: “I mean... I kind of get it though? Like, there are people who think selling action is weak. ‘Real’ players play their own roll. I see it on Twitter all the time. ‘If you need to sell, you’re playing too high.’ ‘Selling is just admitting you can’t afford it.’ There’s a whole crowd that thinks it’s a point of pride to never sell a piece.”

Uncle Tau: (sound of a heavy weight being set down very deliberately) “Bob. I need you to understand something about that ‘pride’ crowd. I need you to understand what they are actually saying, even though they don’t know they’re saying it.”

“They think there is an objective, fixed value to a tournament entry, and that if you sell it for less than that value, you are losing something. They believe in what economists call a Labor Theory of Value: ‘I put in the hours, I studied the ranges, I ground the volume — therefore the output of my labor has a fixed, intrinsic worth. Selling below that worth is giving away what’s mine.’”

Bob: “I mean, that doesn’t sound crazy?”

Uncle Tau: “It doesn’t sound crazy until you remember one thing: poker is a negative-sum game.“

(Silence.)

“Bob, what does a poker player produce? What does he manufacture? What commodity does he create that exists in the world after he stands up from the table?”

Bob: “...”

Uncle Tau: “Nothing. Zero. Poker players do not create value. They redistribute it. And they redistribute it in a system where the house takes rake out of every pot, every tournament, every entry. The total pool of money shrinks with every hand dealt. There is no product. There is no output. There is no widget rolling off the assembly line. Every dollar Roman wins is a dollar another player lost — minus rake.”

“Now, in a Labor Theory of Value — the framework the ‘no sell’ crowd is unconsciously using — value comes from labor. You work, you produce, your output has worth. This is the foundation of Marxist economics. And do you know what Marxist economics has to say about a person who sits at a table, produces nothing, and extracts money from a negative-sum redistribution game?”

Bob: “...nothing good?”

Uncle Tau: “He is a parasite. He is a speculator. He is an unproductive element extracting rent from the system without contributing labor that creates real value. In any honest application of the Labor Theory of Value, poker players are not workers — they are leeches. Under a communist Labor Theory framework, every single one of us gets sent to the gulag. Not metaphorically. Actually. The Soviets did this. Gamblers, speculators, anyone who made money without producing a tangible good — they were classified as parasites on the working class.”

“So when the ‘no sell for pride’ crowd says, ‘I earned this edge with my labor, and I refuse to give it away,’ they are — unknowingly — adopting the one economic framework on earth that says their entire profession is illegitimate. They are borrowing the language of the system that would literally imprison them for what they do.”

Sam: (leaning back in his chair) “That’s... actually hilarious.”

Uncle Tau: “It’s not funny. It’s dangerous. Because if you follow the logic all the way down, it destroys everything.”

“The only reason poker players can exist as professionals — the only reason staking exists, the only reason selling action exists, the only reason any of us can justify sitting at a table and calling it a career — is subjective value. The Austrian economists — Menger, Mises, Hayek — figured this out 150 years ago. Value is not determined by the labor that went into producing something. Value is determined by the individual valuation of each party in a voluntary exchange.“

“In a subjective value framework, poker is not parasitic. It is a market. Players are providing entertainment, liquidity, competition. The rec player values the thrill of the game more than the buy-in he’s likely to lose. The pro values the expected return more than the time he’s investing. Both parties enter voluntarily. Both parties walk away having gained something by their own subjective assessment. That is a legitimate market. That is how all markets work.”

“And selling action is just another layer of this same market. When Roman sells 40% of his $530 package at a 1.1 markup, Roman values variance reduction more than he values that 40% of his expected payout. The buyer values expected return more than they value the cash sitting in their account. Both parties walk away better off by their own subjective assessment. Nobody is losing. Nobody is being cheated. A voluntary transaction occurred because two people valued the same asset differently.”

“This is not a flaw in the system. This is the system. The entire staking economy, the entire swap market, every single action sale that has ever happened in poker — all of it depends on the fact that different people assign different values to the same piece of variance. Remove subjective value, and everything collapses. Not just action selling. Poker itself.”

Bob: “So the ‘never sell’ crowd...”

Uncle Tau: “The ‘never sell’ crowd is borrowing a framework from an ideology that would shut down every cardroom on the planet and put every one of us in a labor camp for being unproductive parasites. They are using the language of the one economic system that says poker has zero value — to protect their ‘pride’ as poker players. The irony is so thick you could stack chips on it.”

“We had all better hope — every single one of us who makes a living moving money around a negative-sum game — that we live in an Austrian economics world. A world of subjective value. A world where voluntary exchange between consenting adults is legitimate, even when no physical product is manufactured. Because if we don’t live in that world? If the Labor Theory crowd is right? Then Roman doesn’t belong in a cell. We all do.“

Sam: “And if you accept subjective value — which you must, to justify your own existence in this game — then selling action is just another voluntary exchange. It’s not weakness. It’s not charity. It’s two rational actors with different utility functions finding a price.”

Uncle Tau: “Which is, incidentally, what Ludwig von Mises called catallactics — the science of exchanges. Every exchange happens because the two parties value the goods differently. If they valued them the same, there would be no reason to trade. The buyer is not doing Roman a favor. He is making an investment. He is buying exposure to a positive-EV asset at a price he considers fair. Roman is selling exposure he doesn’t need at a price that improves his geometric mean. Both are acting in naked self-interest. This is the beauty of markets.”

Bob: “So the ‘never sell’ crowd is basically saying...”

Uncle Tau: “They are saying: ‘I would rather suffer the full geometric drag of an unhedged multiplicative process in a negative-sum game than allow another human being to profit from a voluntary exchange with me.’ And they call this pride. I call it the fastest route to the gulag — ideological and financial.”

Sam: “And for Roman’s situation specifically — he has to sell. Not because he’s weak. Because selling is rebalancing. It’s Shannon’s Demon. It’s the mechanism that converts destructive variance into harvested premium. Without it, he’s stuck in a raw multiplicative grind that will take decades. With it, the math converges in months.”

“Sometimes you have to take the bullet, Tau. Sometimes you let other people make money — even at your own expense — because the network effect of generosity compounds faster than the network effect of stubbornness. Roman selling action below his EV isn’t charity. It’s infrastructure. It’s creating a market around himself. And the market, if you trust subjective value theory — which you’d better, because if you don’t, the entire poker economy is a hallucination — the market will set the right price.”

Uncle Tau: (long pause. Sound of a towel being thrown over a barbell.) “That... is actually not terrible. You may have become smarter in that cell.”

Sam: “Fourteen months of solitary confinement and a potato battery will do that to a man.”

Bob: “So what’s the plan?”

Sam: “The plan has two parts.”

“Part one: I fly to The Accountant. I bring my Finnish bank statements. I bring a spreadsheet that shows what Roman’s earn rate looks like with selling versus without. I show him the geometric mean of both paths. And I tell him two things: ‘Your boy Roman will pay you back in 18 months with selling, or 18 years without. Pick one.’ And: ‘The buyers who purchase Roman’s action will make money. They will tell their friends. Roman’s market grows. His volume grows. You get paid faster. This is not charity. This is how markets work.’”

“Part two: when Roman gets out, he comes to Helsinki. He joins my stable. He coaches.”

Bob: “Your... stable?”

Sam: (the slightest hint of a smile — the first one Bob has seen since Sam got back) “I’ve been building something. Six players. All Finnish. All disciplined. All operating out of this building. We share the sauna. We share the grind station. We do review sessions at 6am before the first bullet fires. Roman knows more about mid-high stakes MTTs than anyone I’ve ever swapped with. His game isn’t broken. His bankroll is broken. Those are different problems.”

Uncle Tau: “You’re building a Finnish poker stable run out of a sauna.”

Sam: “I’m building a Finnish poker stable run out of a sauna. The Finnish Sauna Mafia, if you will. Roman coaches. Roman sells action through the stable’s pool. The stable handles the variance distribution — we cross-collateralize, we rebalance, we run Shannon’s Demon on the entire portfolio. Roman’s geometric mean goes through the roof. The Accountant gets paid. Roman gets free. And when he’s free, he has a home, a grind station, a coaching job, and six Finnish players who owe him their careers.”

Uncle Tau: “And if The Accountant says no to part one?”

Sam: “Then he doesn’t believe in subjective value. And if he doesn’t believe in subjective value, then he also doesn’t believe that the $5 million Roman already paid him was a legitimate transaction. He can’t have it both ways.”

Bob: “I hate economics.”

Sam: “Economics doesn’t care, Bob. But the Finnish Sauna Mafia does. We take care of our own.”

The Lesson

Roman’s prison is not the cell. The cell has WiFi and a solar panel. The prison is The Accountant’s rules — rules built on an additive understanding of a multiplicative game.

In this multiplicative world:

The geometric mean rules, not the arithmetic mean. Volatility is not neutral — it destroys growth. The more volatile your path, the further your geometric mean falls below your arithmetic expectation. The variance itself is eating the returns.

Shannon’s Demon is the antidote. Selling action, swapping pieces, hedging your variance — these are not signs of weakness. They are rebalancing. Shannon showed that you can extract positive growth from volatility by rebalancing a portfolio. Every time a player sells action at a markup, they are running Shannon’s Demon on their own career — converting destructive variance into harvested premium. Ban rebalancing, as The Accountant has, and you force a player to eat the full geometric drag of an unhedged multiplicative process. It is the mathematical equivalent of tying someone’s hands behind their back and asking them to swim.

Loose calls early cannot outrun the math — even if they preserve the mean. Even in the most generous scenario — same arithmetic mean, reshaped into a more extreme lottery — the higher variance pushes the geometric growth rate down. The formula is unforgiving: geometric growth rate equals arithmetic mean minus half the variance. Same mean, more variance, lower growth. Your bankroll compounds slower. Kelly says to bet smaller. You need a bigger bankroll for the same stakes, or you drop down and earn less in dollar terms. To preserve your original geometric growth rate, you would need to significantly increase your ROI to offset the added variance — and the edge gained from a big stack in level 3 comes nowhere close. In reality, the mean drops too. Double punishment: lower mean and higher variance, both hammering the geometric growth rate from opposite directions.

Poker is negative-sum. Nobody creates anything. There is no labor value. Every dollar won is a dollar lost by someone else, minus rake. You are either getting money out of the system or donating into it. In a Labor Theory of Value framework — the framework the “never sell for pride” crowd unconsciously adopts — a negative-sum game where no product is manufactured has no legitimate participants. Everyone at the table is a parasite. Everyone gets sent to the gulag. The only economic framework that justifies poker as a profession is subjective value: the Austrian school, Menger, Mises, Hayek. Value is not intrinsic to the labor — it is determined by what each party in a voluntary exchange is willing to pay. The rec player values entertainment. The pro values expected return. The action buyer values exposure to a positive-EV asset. The action seller values variance reduction. Every transaction in poker — from the first buy-in to the last swap — only makes sense if you accept subjective value. And if you accept subjective value, then selling action is not giving anything away. It is a voluntary exchange between rational actors with different utility functions, and both sides walk away better off by their own assessment. The “no sell” crowd is running the one economic framework that would imprison them for their profession, while calling it pride. We had all better hope we live in an Austrian economics world — because if we don’t, Roman isn’t the only one in a cell.

Roman will get out. The question is whether The Accountant learns the math before Roman’s laptop battery dies for good. And when he does get out, there’s a sauna in Helsinki with his name on it, a coaching chair waiting, and six Finnish grinders who need someone to teach them what a 2000 buy-in downswing actually feels like.

Free Roman.

Thanks for reading Muchomota! Next week: Sam flies to meet The Accountant. He brings a whiteboard, a spreadsheet, and a bag of oranges. The Accountant is not convinced.